The TV and sports media world is essentially still operating on a measurement framework built for a world where you had no choice but to estimate. That world is ending.

For decades, the sports media industry has operated on a gentleman’s agreement with the truth. Broadcasters reported numbers. Advertisers accepted them. Billions of dollars changed hands. And somewhere in the gap between what was claimed and what was verifiable, everyone looked the other way because the alternative — demanding actual proof — would have broken a system that was working reasonably well for most of the people at the table.

That gap is closing. And when it closes completely, the reckoning for sports media economics will be significant.

The Estimation Economy

To understand where we are, you have to understand how television measurement was built. Nielsen’s panel methodology — the foundation of TV ratings for over 70 years — was an engineering solution to an impossible problem. You cannot count every viewer. So you sample a representative group, extrapolate to the broader population, and report the result as if it were a count. For a world with three broadcast networks and no alternative, it was reasonable. Imperfect, but reasonable.

The problem is that the media landscape has fractured into hundreds of platforms, streaming services, social channels, and devices — and the measurement infrastructure has not kept pace. What has kept pace is the money. Sports media rights fees have exploded. Ad rates have held or climbed. Carriage deals have been negotiated using viewership claims that remain, at their core, educated guesses dressed in the language of precision.

The digital advertising industry spent the last 15+ years building a fundamentally different model: verified, logged, session-level data. A view is a view because a server recorded it. An impression is traceable. A completion rate is a calculation, not an extrapolation. It is not a perfect system — anyone who has run campaigns across platforms knows that “impression” still means different things in different contexts — but the directional difference from television measurement is enormous.

Sports media has never had to live by those rules. Until now.

Nielsen’s Inconvenient Transition

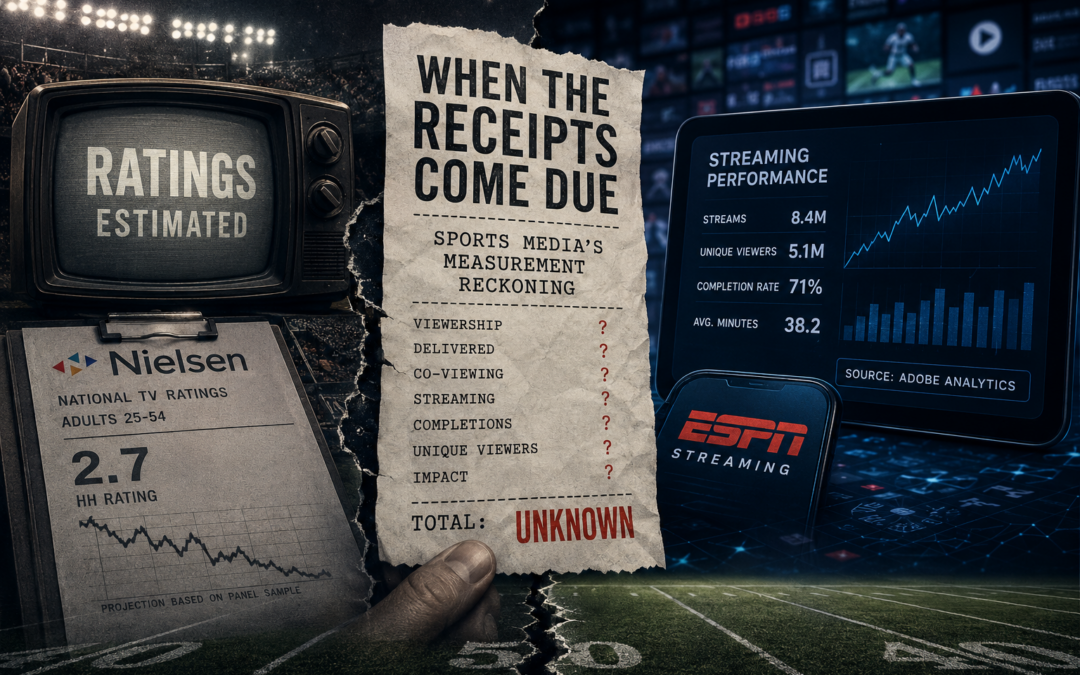

In fall 2025, Nielsen rolled out what it calls “Big Data + Panel” as the official currency for TV measurement — an attempt to modernize by blending traditional panel data with larger datasets from set-top boxes and connected devices. On paper, it sounds like progress. In practice, it has exposed more problems than it has solved.

The Media Rating Council, the independent body that accredits audience measurement services, flagged significant concerns almost immediately. Demographic measurement showed unusual instability — total day impressions for adults 25-54 declined by more than 10% on average during the first half of 2025 compared to the prior year, a drop that had less to do with actual audience behavior and more to do with modeling errors in the new methodology. The MRC’s review of Nielsen’s accreditation status remained unresolved well into 2026, with the organization noting that Nielsen had made “notable progress” on some concerns but that final evaluation could not yet be completed.

More damaging for the sports media world specifically: the NFL’s own chief data and analytics officer publicly stated that Nielsen is “systematically undercounting” millions of viewers, citing inadequate measurement of co-viewing and the fact that Big Data + Panel still lacks first-party data from the majority of NFL rightsholders — including ESPN, Fox, NBC, and CBS. The league that generates the most valuable sports media inventory in the world does not trust the numbers being reported for its own games.

ESPN, for its part, has been working with VideoAmp as an alternative measurement partner. Nielsen has sued VideoAmp multiple times for patent infringement. This is the state of the industry’s measurement infrastructure in 2026.

The Streaming Black Box

The linear television problem is at least a known and documented one. The streaming measurement problem is worse, because it is largely invisible.

ESPN launched its standalone streaming platform in August 2025. Its viewership metrics for that platform are reported primarily through Adobe Analytics — an internal measurement tool, not an independently verified third-party count. When ESPN reports combined viewership figures that blend linear and streaming audiences, the streaming component is essentially self-reported. The methodology is not independently audited in the same way linear ratings are, and the definition of what constitutes a “view” on a streaming platform is not standardized across the industry.

This is the digital world’s oldest problem imported into a new context. Served impression versus viewed impression. A stream initiated versus a stream completed. A unique viewer versus a session. These distinctions matter enormously for understanding actual delivery, and sports media has been slow — deliberately or otherwise — to make them clearly.

The result is that a brand buying a streaming sports placement is often purchasing something whose actual delivery cannot be verified with the same rigor the brand would demand from a digital video buy, a programmatic placement, or even a social media campaign. The premium, however, remains.

The Conditioned Brand Premium

Here is where the economics become genuinely difficult to justify.

Sports media — and ESPN in particular — commands advertising rates that have become substantially decoupled from verifiable delivery. This is not a criticism unique to sports; it applies broadly to prestige television, live events, and any media context where the brand association itself is treated as part of the value. Buyers pay not just for the audience but for the implied credibility of the placement.

That premium is real and it has legitimate foundations. Live sports draws engaged audiences. Brand safety is relatively high. The cultural relevance of major sporting events is undeniable. These are genuine values, and any honest accounting of media placement has to weigh them.

But the premium has also become a kind of institutional inertia. Media buyers at large agencies are evaluated on defensibility, not efficiency. A budget allocation to a major sports network is a safe decision regardless of what the verified CPM math shows. An allocation to a newer, digitally-native platform with superior verified metrics requires justification if anything goes sideways. The incentive structure protects incumbents even when the data does not.

This is not a rational market. It is a credentialed one — and credentials and verification are not the same thing.

Impression vs. Viewer: The Definition That Costs Advertisers

The most important question a brand-side marketer can ask any media partner — traditional or digital — is deceptively simple: What exactly are you counting?

In digital media, the standards, while imperfect, are at least debated openly. The IAB has definitions. Viewability standards exist. Completion rates are measurable. Unique reach can be estimated with reasonable methodology. When a platform reports 10 million impressions, there is at least a framework for interrogating what that means.

In television, the word “impression” has historically meant an estimated exposure derived from a panel extrapolation. It is not a count. It is a model output. And in the current transitional period — where Nielsen’s new methodology is under active MRC review, where streaming numbers are self-reported, and where major rights holders are publicly contesting the numbers — the gap between claimed and verifiable delivery may be wider than it has been in decades.

The platforms winning this ambiguity are the ones with the strongest brand conditioning. The platforms losing are the ones with the most honest numbers — because honest, verified numbers invite comparison, and comparison is dangerous when your rates are built on estimation.

Meanwhile, digital and social platforms that can demonstrate verified views, completion rates above 100% driven by genuine re-watch behavior, and self-selected audiences with high category intent are often competing for budgets at a fraction of the CPM of their less-verifiable counterparts. The math does not add up. It persists because the buying culture has not yet demanded that it do so.

What Forces the Change

The technology to verify viewership at scale already largely exists. What has been missing is the market pressure to demand it.

That pressure is building from multiple directions simultaneously. Alternative measurement companies — VideoAmp, iSpot, Comscore — have received formal recognition from the Joint Industry Committee and are actively pursuing advertiser relationships that bypass Nielsen entirely. Major brands are running their own cross-platform attribution studies and beginning to see the CPM discrepancy in their own data. The NFL is publicly pushing for better measurement of its own product. The MRC is applying pressure on Nielsen to either fix its methodology or face accreditation consequences.

The moment that will accelerate everything is when a major advertiser — or a major agency with fiduciary exposure — publishes or leaks a verified cross-platform study showing what they actually got for their money versus what was sold to them. That study exists somewhere. When it becomes public, the conversation will shift from theoretical to contractual.

At that point, every media partner will be asked to produce receipts. The partners with verified, logged, session-level data will hand them over without hesitation. The partners whose numbers are built on estimation, extrapolation, and self-reporting will face a very different kind of negotiation.

What Brand Marketers Should Be Demanding Now

You do not have to wait for the industry reckoning to start asking better questions. Any media partner, regardless of platform or prestige, should be able to answer the following clearly:

What exactly is a “view” in your reporting? Is it a served impression, a 3-second view, a completed view? Is it unique per user or total plays?

What is your completion rate? And is that metric available at the individual content level, not just as a blended average?

Is your measurement independently verified? By whom, under what methodology, and is that methodology publicly available?

What is the verified CPM? Not the rate card CPM — the actual cost per verified, completed, unique view delivered to your target audience.

Can you segment the audience? Can you show me who watched, not just how many?

These are standard questions in digital media buying. They should be standard everywhere. The fact that they are still considered aggressive or unusual in sports media contexts tells you everything about how far the reckoning still has to travel.

The Reckoning’s Timeline

The sports media industry will not collapse under the weight of measurement reform. The underlying product — live sports, cultural moments, passionate audiences — is genuinely valuable and will remain so. Rights fees will not go to zero. ESPN will not disappear.

What will change is the pricing logic. When verified delivery becomes the standard currency, media investments will increasingly flow toward platforms that can demonstrate what they actually delivered — not what a panel extrapolated, not what an internal analytics tool reported, not what a blended linear-plus-streaming figure obscured.

The brands that start demanding verification now will have a significant advantage in that transition. They will have built relationships with partners who can prove their value, developed internal benchmarks for what verified delivery actually costs, and avoided years of overpaying for impressions that were never quite what they were sold as.

The receipts are coming. The only question is whether you’re the one asking for them or the one hoping nobody does.

This article reflects analysis of publicly available industry data and reporting from Nielsen, the Media Rating Council, Sports Media Watch, Marketing Brew, and other trade sources.