Distribution Is the New Currency – Visibility the Battleground

Executive Snapshot – Key Q1 2026 / End-2025 Benchmarks

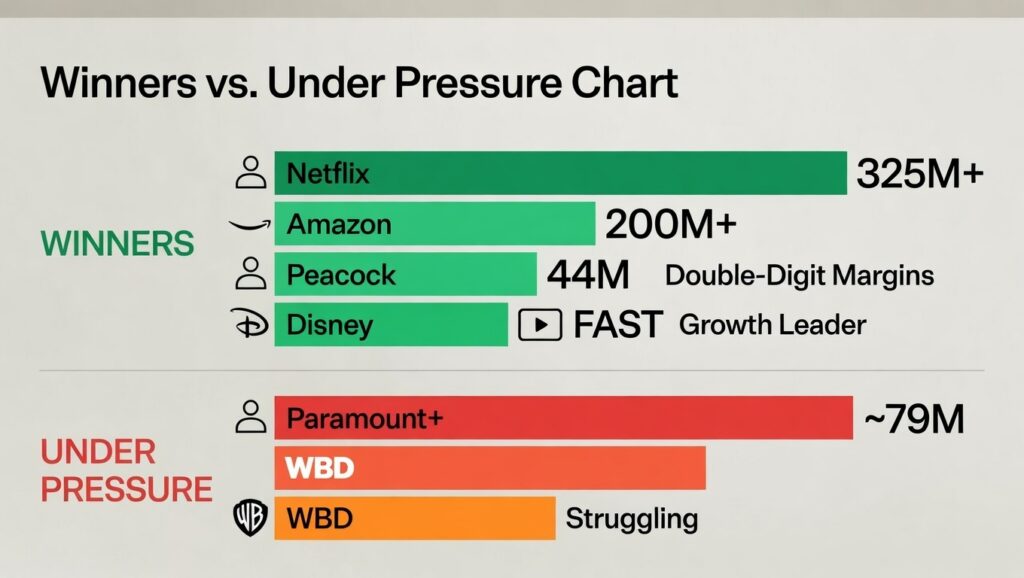

- Netflix: >325 million paid memberships (end-2025), full-year revenue ~$45.2B (+16% YoY), ad revenue >$1.5B and doubling trajectory in 2026. Serves audience nearing 1B globally.

- Disney (Disney+/Hulu): Streaming profitability climbing (e.g., $450M operating income in Q1 FY2026, margins nearing double digits); phased out granular sub reporting to focus on revenue/margins; combined subs last reported ~196M (end-FY2025).

- Paramount+: ~79 million subs (end-2025, excluding free trials), DTC revenue +10-17% in recent quarters; post-merger guidance targets $30B total revenue in 2026.

- Peacock: 44 million paid subs (end-2025, +22% YoY), driven by sports/live.

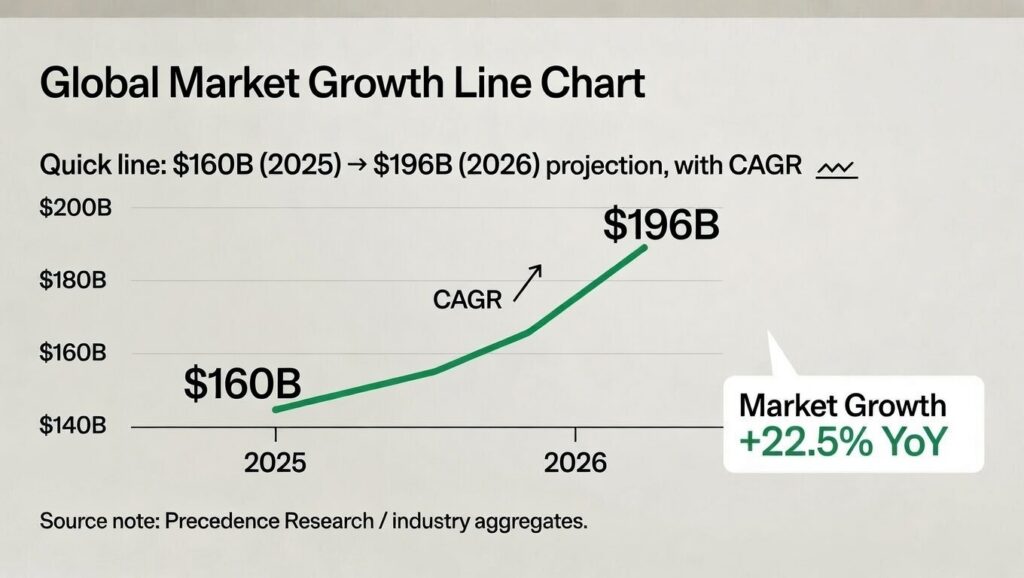

- Global Video Streaming Market: ~$160B in 2025 → projected ~$196B in 2026 (CAGR ~18-21%, fueled by FAST/AVOD explosion).

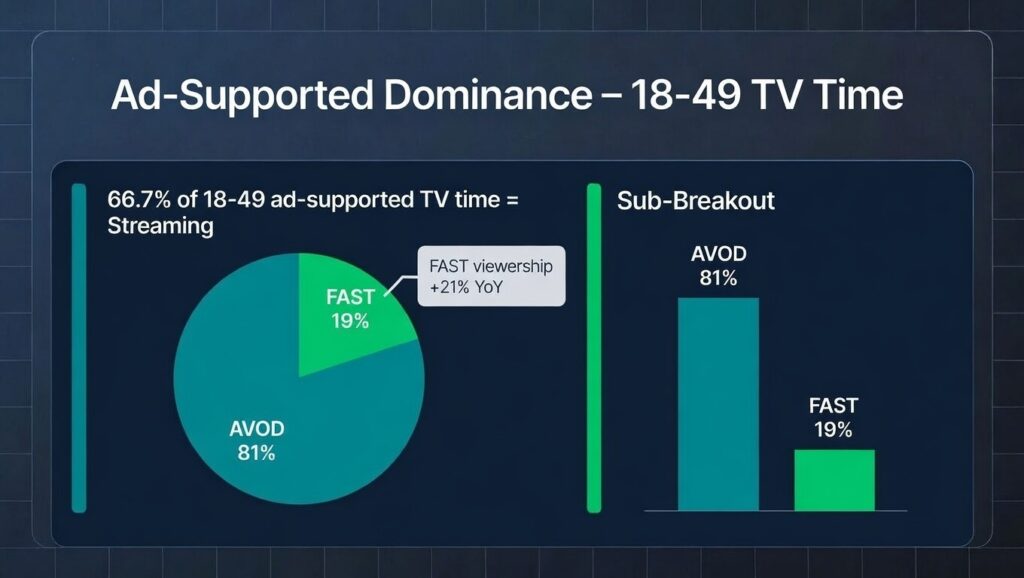

- Ad-Supported Dominance: Streaming now 66.7% of ad-supported TV time for 18-49s; FAST viewership +21% YoY in Q4 2025; >70% of key-market TV time ad-supported.

The Big Shift: Distribution Over Platforms

Content is abundant. Attention is scarce. Distribution is everything. The subscriber-chase era (2020–2025) is dead. In 2026, winners control pathways to audiences—not just libraries. Bundle fatigue, algorithmic silos, and exploding FAST/CTV options fragment discovery. Independent creators and brands face the harsh truth: Publishing content ≠ getting discovered. Visibility is the new moat.

Winners and Those Holding Steady

- Netflix – The profitability king: Hybrid sub + ads model locked in, with ad tier now ~35% of subs. Scale + originals + global push keep it dominant.

- Amazon Prime Video – Bundled ecosystem + sports/live events + ad-tier momentum make it a quiet powerhouse.

- Peacock – Sports rights (NBA, Olympics) fuel 44M subs; ad-supported growth narrows losses.

- Disney – Profitability trajectory strong (double-digit margins approaching); Hulu integration into Disney+ reduces churn, boosts time-spent.

- FAST/CTV players (Tubi, Pluto, Roku Channel) – Explosive: 21% YoY viewership growth in Q4 2025; free/frictionless access captures cord-cutters and younger demos.

Under Pressure

- Paramount Skydance – Modest DTC gains post-merger, but legacy TV drag and rights costs persist; 2026 revenue target $30B requires discipline.

- Warner Bros. Discovery – Ongoing restructuring; streaming profitability improving but content spend scrutiny high.

- Legacy cable/broadcast – Accelerating decline as sports migrates hybrid/streaming.

The Rise of Ad-Supported Everything

Ad tiers now drive most SVOD growth. Consumers embrace the trade-off: lower/no cost for targeted ads. Key trends:

- Programmatic precision on CTV/FAST delivers measurable ROI.

- FAST as discovery engine for niche/sports/news.

- Bundling evolves to integrated packs (sports + entertainment).

- Attention monetization > volume: Platforms prioritize engagement over raw subs.

Creator Reality in 2026

For independents and brands:

- Algorithms favor incumbents and paid promo.

- Libraries balloon → discoverability bottleneck worsens.

- Repeatable audience growth demands ownership + direct relationships, not platform dependency.

Emerging models prioritizing creator tools, transparent monetization, and equitable distribution are gaining traction—addressing the core challenge: turning visibility into sustainable revenue.

What’s Next: Q3 2026 Outlook

- Consolidation wave (more mergers/bundles).

- AI-driven personalization/discovery reshaping algorithms.

- Next ad phase: Higher loads, interactive formats, commerce integration.

- Sports fragmentation accelerates hybrid deals.

From WingDing®: Building for the Shift

At WingDing®, we’re betting on creator-owned distribution. Tools like Creator Labs (idea validation + development) and the Creator Guild (community, monetization pathways) help independents build direct audiences—bypassing algorithmic gatekeepers for long-term control.

Final Thought

2026 isn’t about who has the most content. It’s about who masters distribution in a post-platform world. Those empowering equitable, scalable pathways to viewers will lead the next era.

Coming Next: Q3 2026

Consolidation, AI-driven discovery, and the next phase of ad-supported streaming.